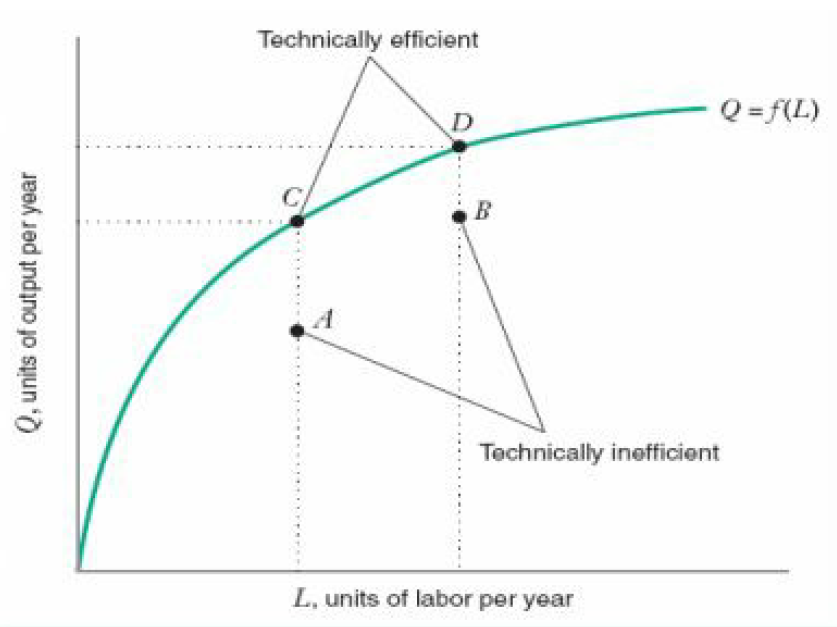

For the given production function, technical efficiency is defined as:

Sets of points relating production function that maximizes output given input (labor) i.e. Q = f(L, K)

Sets of points relating production function that produces less output than possible for a given set of input (labor) i.e. Q < f(L, K)

Use of imported technology

None of the above

Correct Answer :

A. Sets of points relating production function that maximizes output given input (labor) i.e. Q = f(L, K)

{Diagram is given below}

Related Questions

According to classical approach, utility can be:

Ranked

Consumed

Expressed in numbers

Cannot be expressed in numbers

The advantage of using indifference curves rather than marginal utilities is:

We do not need to attach util values to consumption

Consumers can attain higher utility

It takes into account how much income the household has

We can determine how much of one good the consumer is willing to sacrifice in order to consume one more unit of another

In the modern theory of costs, the level of production which the firm considers feasible is known as:

Input factor

Heavy factor

Output factor

Load factor

At the point where a straight line demand curve meets the quantity axis (x-axis), elasticity of demand is:

Equal to zero

Equal to one

Equal to infinite

More than one

Price elasticity of demand can be measured in the following way:

Percentage change in quantity demanded of a commodity divided by percentage change in price of that commodity

Change in quantity demanded of a commodity divided by change in price of that commodity

Percentage change in price of a commodity divided by percentage change in quantity demanded of that commodity

None of that commodity

Which is the first-order condition for the profit of a firm to be maximum?

AC=MR

MC=MR

MR=AR

AC=AR

Nash Equilibrium is stable:

They involve dominant strategies

They involves constant-sum games

Once the strategies are chosen, no player has an incentive to deviate unilaterally from them

None of the above

The study of economics just in theoretical way is called:

Positive Economics

Normative Economics

Micro Economics

Development Economics

Kinked Demand Curve is consistent with which one of the following market situations?

Pure competition

Pure monopoly

Oligopoly

Monopolistic competition

J.R.Hicks was:

Neo-classical economist

Classical economist

Keynesian economist

Post-Keynesian economist

The cournot model is a model of:

Instable equilibrium

Stable equilibrium

Constant equilibrium

Fluctuating equilibrium

In real life, brand loyalty is a barrier to:

Enter the new firms

Exit the new firms

Both a and b

None of the above

In second degree price discrimination, monopolist takes away :

All of the consumer surplus

All of the producer surplus

Some part of the consumer surplus

None of them

At the point where the straight line from the origin is tangent to the TC curve, AC is:

Maximum

Minimum

Equal

Lower

In Edgeworth model, if price falls below competitive price, the demand is:

More than maximum output

More than minimum output

Less than maximum output

Less than minimum output

The number of sellers in oligopoly are:

Two

Many

Four

Very few

Cournot equilibrium is attained where two reaction curves:

Repel each other

Represent each other

Intersect each other

None of the above

LMC represents change in LTC (long-run total cost) due to producing an additional unit of a good while the fixed and variable factors:

Cannot be changed

Can be changed

Can partially be changed

None of the above

Utility means:

The want- satisfying power of a commodity

Usefulness of commodity

Eating of commodity

None of these

In Edgeworth model, prices oscillate between:

Firms and industry price

Monopoly and duopoly price

Competitive and monopoly price

None of the above

In dominant price leadership model, the small firms are like:

monopolistic firms

monopoly

competitive firms

none of the above

Moving along an indifference curve leaves the consumer:

Better off

Worse off

Neither better nor worse off

None of the above

In cournot model, at equuilibrium when MC = MR, the elasticity of demand is:

equal to one

zero

negative

equal to 2

The concept of period refers to:

A specific duration of time

A varying duration of time

A duration of time which permits necessary adjustments

A period with calculated intervals

The firm producing at the minimum point of the AC curve is said to be:

Operating under diminishing cost

Making optimum use of plant capacity

Operating at excess capacity

Operating under increasing costs

In second degree price discrimination, monopolist takes away :

All of the consumer surplus

All of the producer surplus

Some part of the consumer surplus

None of them

Cross-elasticity of demand or cross-price elasticity between two complements will be:

Negative

Positive

Infinite

Zero

In substitution effect and income effect:

The substitution effect is more certain

The income effect is more certain

The substitution effect is uncertain

The income effect is always positive

Which of the following formula determine the income elasticity of demand?:

Proportionate change in demand Proportionate change in price

Proportional change in the purchase of Y Proportional change in the price of X

Proportionate change in demand Proportionate change in income

Proportionate change in demand Proportionate change in price

Price-taker firms:

Advertise to increase the demand for their product

Do not advertise, because most advertising is wasteful

Do not advertise because they can sell as much as they want at the current price

Who advertise will get more profits than those who do not