Which of the following is called Gossens first law?

Law of production

The Law of Equi-Marginal Utility

The Law of Diminishing Marginal Utility

Law of Variable Proportions

Correct Answer :

C. The Law of Diminishing Marginal Utility

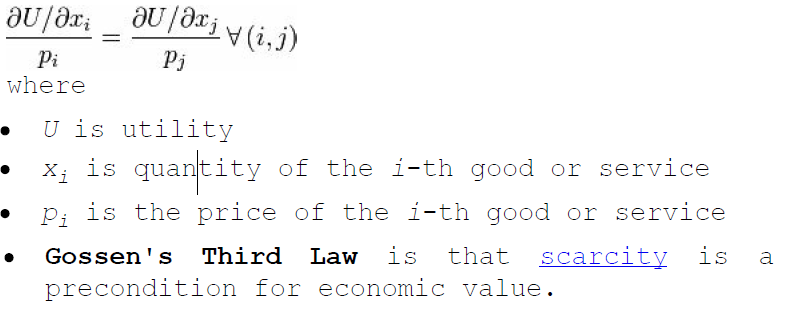

Gossen's laws, named for Hermann Heinrich Gossen (1810 - 1858), are three ostensible laws of economics: Gossen's First Law is the law of diminishing marginal utility: that marginal utilities are diminishing across the ranges relevant to decision-making. Gossen's Second Law, which presumes that utility is at least weakly quantified, is that in equilibrium an agent will allocate expenditures so that the ratio of marginal utility to price (marginal cost of acquisition) is equal across all goods and services.

Related Questions

At final equilibrium in cournot model, each firm sells:

1/2 of the total market demand

1/4 of the total market demand

1/3 of the total market demand

None of the above

In dominant price leadership model, the small firms are like:

monopolistic firms

monopoly

competitive firms

none of the above

The model which gives us information about price and output changes in different periods is:

Stable cobweb model

Perpetual oscillation

Both(a) and(b)

None of them

The number of sellers in oligopoly is:

Two

One

Very large

A few

The pay-off matrix shows:

Possible outcomes

Possible benefits

Possible losses

None of them

The production function of homogeneous of degree one (n=1) is also called:

Linearly homogeneous

Zero homogeneous

Infinite homogeneous

None of the above

A high value of cross-elasticity indicates that the two commodities are:

Very good substitutes

Poor substitutes

Good complements

Poor complements

The isoquant approach is based upon:

One output

One input

Two outputs

Two inputs

A market demand curve presumes that:

All consumers are alike

Incomes of all consumers is the same

Tastes of all consumers are the same

Consumers differ in taste, incomes and other matters

Cross-elasticity of demand or cross-price elasticity between two perfect complements will be:

Negative

Positive

Infinite

Negative infinite

An indifference curve normally slopes downward from:

Left to right

Right to left

Both of them

None of them

Indifference curve approach (ordinal approach) is superior to utility approach (cardinal approach) because:

In ordinal approach we can separate the income effect from the substitution effect of a price change

In ordinal approach we can study the consumer behavior more closely

In ordinal approach the consumer is assumed more rational

In ordinal approach the consumer has more income

Production indifference curve (isoquant) is a curve which shows:

Equal level of output

Unequal level of outputs

Equal level of inputs

Unequal level of inputs

In repeated game, the Prisoners Dillemma can have a:

Non-cooperative outcome

Cooperative outcome

Dominant behavior

Recessive behavior

In general, most of the production functions measure:

The productivity of factors of production

The relation between the factors of production

The economies of scale

The relations between change in physical inputs and physical output

Neutral Technological Progress can be defined as:

Technological progress that causes to raise the marginal product of capital and labor in the same proportion

Technological progress that causes the marginal product of capital to increase relative to the marginal product of labor

Technological progress that causes the marginal product of labor to increase relative to the marginal product of capital

None of the above

With firms having cost differences under perfect competition, a firm, which earns normal profit in the long-run is called:

An optimum firm

A representative firm

An oxford firm

A marginal firm

When price decreases and with it the total outlay on a commodity also decreases, it is a case of:

Perfect elasticity (infinitely elastic)

Relative elasticity (greater than one elasticity)

Perfect inelasticity (zero elasticity)

Relative inelasticity (less than one elasticity)

If the slope of the isoquant is equal to the slope of isocost, then isoquant is:

Concave to the origin

Convex to the origin

Tangent to the origin

None of the above

Any expansion in output by a firm in the short period will always reduce the:

Average variable cost

Average fixed cost

Both average fixed and variable cost

None of the above

If the price of product increases and in the result the demand for product B also increases then:

A and B are substitute goods

A and B are complementary goods

A is inferior to B

A is superior to B

Microeconomics deals with the:

Allocation of resources of the economy as between production of different goods and services

Determination of prices of goods and services

Behavior of industrial decision makers

All of the above

Marginal Utility (MU) curve is always:

Rising

Falling

Parallel to X-axis

Parallel to Y-axis

We can obtain consumers demand curve from:

Income Consumption Curve (ICC)

Engels Curve

Price Consumption Curve (PCC)

Production Possibility Curve (PPC)

One way the government can induce a monopolist to expand his output is by imposing:

A specific tax on the monopolists output

A price ceiling that make the monopolist lower his price

A price floor that make the monopolist raise his price

A heavy tax on the monopolists profit

Which of the following pairs of commodities is an example of substitutes?

Tea and sugar

Tea and coffee

Pen and ink

Shirt and trousers

In non-collusive oligopoly firms enter into:

Secret agreements

No secret agreements

Bad habits

None of the above

In second degree price discrimination, monopolist takes away :

All of the consumer surplus

All of the producer surplus

Some part of the consumer surplus

None of them

Robbins definition of economics was criticised by:

Alfred Marshal

Adam Smith

J.B.Clark

Hicks, Longe and Durbin

In monopolistic competition, the firms follow:

Exotic behavior

Sympathetic behavior

Myopia behavior

Regular behavior